How far might broadband funding go? Estimating state-level deployment programs, and v2 national model

BEAD provides enough funding to reach all the unserved. Some states still have a hard road.

In a previous post, I estimated how far the BEAD broadband funding might go in closing the Digital Divide. With this updated model, the national story is the same: after you factor in existing funding programs and private capital matches, there is plenty of money in BEAD to reach all of the unserved and reach far into the underserved. Maybe more interesting are the state-level stories. Due to dramatic differences in cost per location to bring new broadband, some states like Kansas will only be able to reach 10% of their un- and underserved, while many states with lower costs will be able to reach all their unserved and all their underserved.

Congress was aware that states with higher costs needed more funding, however the IIJA only allocates 10% of the $42.45 billion based on the number of “high cost locations” in a state. For example, Kansas is entitled to the same $100 million as every state. According to the latest FCC data they have 0.21% of the national unserved locations which entitles them to an additional $68 million. Kansas has relatively higher costs, so they make up 0.77% of the high-cost locations nationally (high cost in my estimates are locations in the top 25% of cost nationally). In the high-cost allocation they add $32.6 million for a total estimated BEAD allocation of $201 million. That money doesn’t go very far when the average location costs $16,100 to reach with fiber. The 10% allocation based on high cost locations does almost nothing to smooth out differences in cost per location across states.

Kansas has something else working against it. All of the funding is allocated based on the number of unserved locations, with underserved locations thought of as side-benefit. In Kansas, just 5% of the estimated 295,000 un- and underserved locations are unserved. So if the goal is to reach the un- and underserved — as I think it should be — Kansas is attempting it with a fraction of the necessary funding.

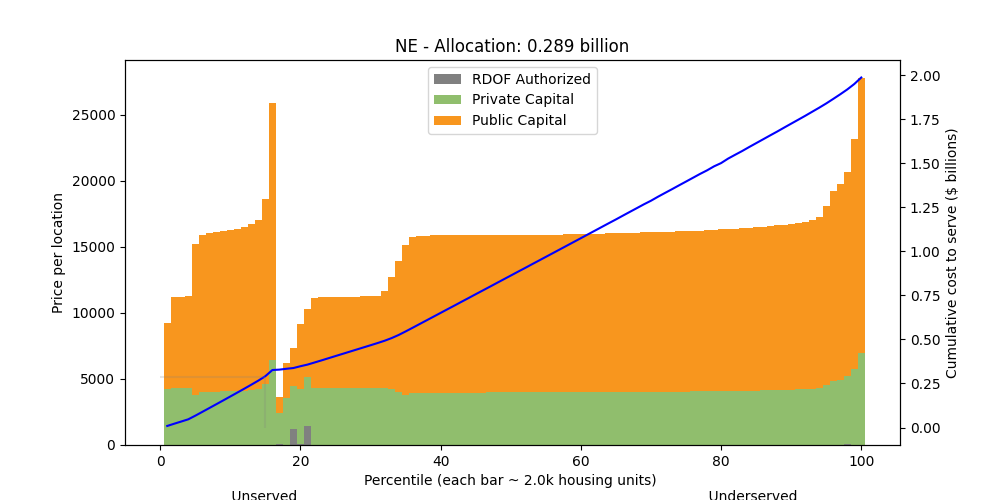

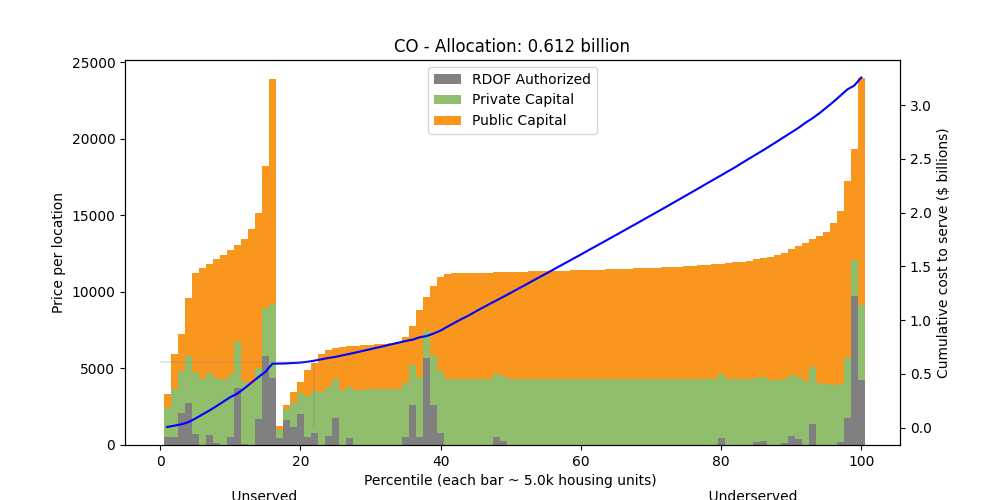

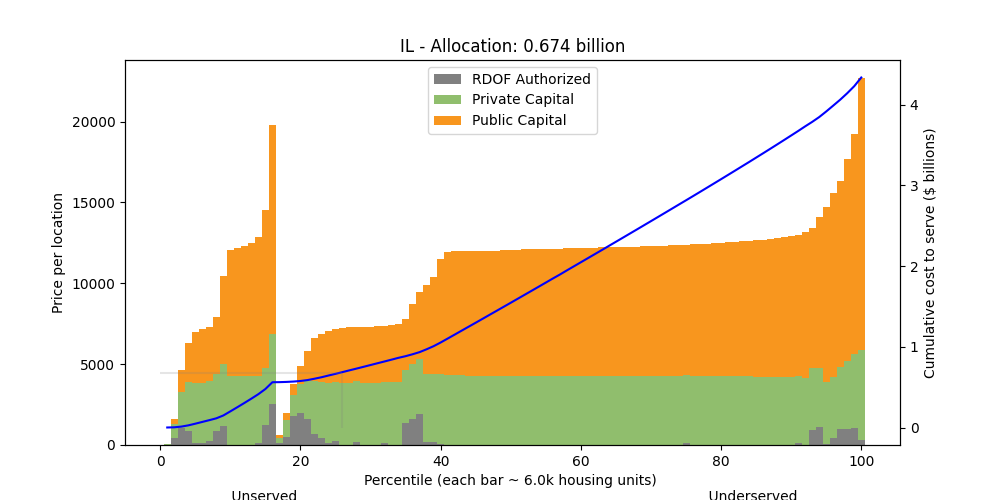

Other states have the same issue, but not quite as bad. Nebraska is estimated to be able to reach 15% of its underserved (avg cost $15.6k/location), Colorado 22% (avg $12.3k/location), Illinois 26% (avg cost $9.4k/location). By contrast, 26 states are estimated to be able to reach 95% or more of the combined unserved and underserved.

{kind=link}

{kind=link}

{kind=link}

Here is a link to the national and state charts. And these are the allocations I used.

There is nothing NTIA can do about this. Allocating 10% based on “high-cost locations” isn’t enough to push money into expensive states. In fact, it’s possible new FCC maps push money the other way: to big states relative to small ones. Even if the new FCC maps find unserved locations that skew rural, rural areas in big states could add more locations than rural areas in small states. Since the allocations are based on each states’s contribution of unserved locations to the national total, more unserved locations could actually shift money towards those big states.

But let’s back out to the national level and look at the big picture including the assumptions that go into this model. This model estimates we can bring fiber broadband to all the unserved for less than $20 billion. It’s a shocking finding, but here are the facts: it uses an average cost for unserved locations of $6,412; 2.4 million (out of 7.6 million estimated unserved) locations have already been authorized for RDOF funding; and private capital should be expected to pick up a sizable part of the tab. Not only that, but by the time we spent all $42.35 billion, we could serve 78% of the underserved as well. Here’s the chart:

Here’s how to read these charts: from the left, we start by funding the least expensive unserved areas. As we move right, the unserved areas get more expensive, until eventually we’ve funded them all. Then we “reset” to start funding the least expensive underserved areas. Each vertical bar represents 1/100th of the total number of housing units that are un- and underserved. With the estimates we’re using there are 23.1 million of those, so with each bar that we pass moving left-to-right we’ve served 231k housing units.

You can think of this model as a list with just two pieces of information: whether a house is un- or underserved, and how much it would cost to bring fiber service to that home. Then we order that list from least expensive to most expensive and bring broadband to those homes until we run out of money.

Un- and underserved Locations

How many housing units (or “broadband serviceable locations”) are without access is one of the critical questions. According to the FCC Form 477 data as of June 30, 2021 there are 3.6 million unserved housing units and 7.5 million underserved housing units. For this model, I’ve doubled those numbers. Since the new FCC maps will include any “broadband serviceable location”, not just housing units, I’ve added 11% to that number. In the RDOF auction, there were 11% more eligible locations than housing units, which I use as an estimate. So there are 7.6 million unserved locations and 15.6 million underserved locations for a total of 23.1 million locations nationally.

How does 23.1 million un- and underserved compare with other numbers about the Digital Divide? Recently, Jim Stegeman, CEO of CostQuest, was asked this question in an interview. Paraphrasing his answer, he said 23-25 million locations don’t have access to technology that would make them served. Another point of comparison is the landmark 2017 study by Paul De Sa at the FCC. Using December 2015 data, he estimates that $80 billion could serve the remaining 14% of unserved locations that existed at the time. That equates to about 22.4 million unserved locations and a cost of $3,571 per location. We have 18% as many unserved locations as there were at that time, and we’ve allocated 53% of the funding they recommended.

While I think there’s emerging consensus that the “Digital Divide” is 23-25 million locations, maybe just above 50 million people, I haven’t seen predictions on the proportion that is unserved vs underserved. I’m not making one here, and instead just doubling the un- and underserved which keeps the proportion the same - 1/3rd unserved and 2/3rds underserved. If the new FCC maps come out with 12 million unserved, obviously it will be more expensive to serve all of them. A bigger “known unknown” is what happens if the distribution across states changes. As I’ve looked at previously, the allocation of BEAD money by state is very sensitive to small changes in unserved locations. For example, even if Kansas’s unserved count goes up by 2.5x, if PA goes up by 4x then Kansas loses.

BEAD grants won’t be used to fund areas that have already been authorized by the FCC for RDOF funding, so we don’t need to worry about those. Those areas are in grey in the chart. Almost 30% of the housing units in unserved areas have already been authorized by RDOF. That’s why the grey section for unserved areas is sizable.

Cost to Serve

It’s important to remember that the new FCC maps will show partially served blocks. The new locations we’ll learn about already have at least one housing unit served. In that sense, they are likely to be cheaper — perhaps significantly — than completely unserved census blocks. By doubling the number of un and underserved housing units we’re copying their cost structure too. Therefore, it’s probable that we’ve overestimated the cost to serve half of these locations.

Of the remaining areas, there’s an expectation that private (or at least non-BEAD) capital will serve as matching funds — the federal government hopes to not have to fund 100% of these projects. In this model, if the cost per location is less than $2,000, I assume private capital needs to bring 70% of the total build cost. If the cost is over $12,000 per location, I assume private capital needs to provide 25% of the build cost, the statutory minimum. The private capital match declines linearly from 70% to 25% between $2,000 and $12,000 per location.

I’ve been critical of parts of the RDOF auction, but one thing it did well was show how much private capital was willing to put towards broadband buildout. Private capital brought more than 90% of the necessary funding in 20% of the locations that were won by providers planning to offer gigabit service. As a reminder, these location were unserved and relatively high cost. If private capital can bring most of the funding during RDOF, let’s find a way to bring the same level of private capital to state-administered grant programs. Of course, if states issue grants after a single round of proposals with no mechanism to make providers compete, this will be easier said than done. It is not as simple as just giving a higher score for applications that offer a "higher match," especially with many states also lacking an independent view of costs...a final important topic that as we'll turn to now.

There’s no doubt — costs have increased since the RDOF auction took place. How much is the harder question. According to the Financial Times quoting Corning’s CEO, fiber prices in the U.S. have gone up 2% this year. Regardless, in this version I’ve increased the cost to serve a location by 25% over the implied price from the RDOF reserve price. Unfortunately, it’s easy to imagine a situation where grantees hand-wave about labor costs, supply chains, and inflation in justifying costs that are many multiples of what they were two years ago. If the price is high enough, the grantee could offer a seemingly high private match against that price, making the grant look good on paper.

The FCC's high cost program has long been based on a detailed national cost model. Although people sometimes take issue with its exact accuracy in any given area, we can safely say that in aggregate it has been proven to serve as a useful starting point for subsidy awards. In both the CAF II and RDOF auction, using the FCC cost model as the basis for setting the initial reserve price, well over 90% of eligible block groups received a bid, and most block groups received many descending bids. In other words, across these nationwide auctions, that cost model was viewed as accurate enough that almost nowhere was it the case that no provider viewed it as a reasonable cost starting point. And, as discussed above, in many areas providers were willing to come down to much lower levels.

With states now playing the same grant awarding role in BEAD, this raises the question of how states without such cost information available will set the starting conditions for their BEAD subgrant awards. Unlike areas such as roads and bridges, few states have extensive independent experience with project construction costs for broadband. All of the results I'm discussing assume that actual state BEAD awards will generally follow a reasonable understanding of project costs.

While the imbalance between expensive states and less expensive states is hard to solve — the allocation formula is written into the law — there are actions we can take on managing costs. A “back-end” process where NTIA evaluates and rejects grants based on costs would be unpopular and probably unworkable. However, a process on the front-end might work. I’d suggest a transparent cost model available to all states and potential grantees as a yardstick against which to measure proposals. In my view, a public cost model could make a significant impact in making this once-in-a-generation funding go as far as possible—possibly bringing broadband all of the unserved, and a lot more.

Thanks to Jon Wilkins at Quadra Partners for thoughtful comments on early drafts of this analysis.